These personal finance statistics will teach you what the average American household has in average savings, average credit score, and how much debt the average American has.

It's no secret that student debt and annual incomes play a huge role in our economy. But did you know these other personal finance statistics for 2022?

How many Americans are financially healthy?

According to the 2022 Wealth & Wellness Index, people's feelings about their financial health are mainly impacted by their income and debt, and savings.

Most workers claimed that rising expenditures and not being paid enough are keeping them from shaking off the impacts of the Covid epidemic, especially as inflation is already eating into salary growth starting in 2021.

By analyzing personal finance statistics – they revealed while workers have received their first genuine salary increases in years, Americans are now facing a rising cost of living expense climbing at its highest rate in over four decades.

According to the 2022 Empower Wealth and Wellness Index, just 34% of Americans considered themselves extremely financially well in the fourth quarter of 2021.

As the data shows, lower-income people continue to confront disproportionate economic challenges, affecting their financial well-being and physical, mental, and emotional well-being at about twice the rate of higher-income people.

More Americans are struggling to keep up with expenses and meet the cost of necessities due to growing costs.

Americans are cutting back on discretionary expenditures and spending more on essentials as inflation fears grow.

Americans believe that salaries have not kept pace with inflation, with lower-income earners bearing the brunt of the blame

The Capital One Insights Centre has released new data to coincide with the second anniversary of the COVID-19 outbreak, demonstrating that the gap between lower and higher earnings continues to increase in the face of growing economic challenges.

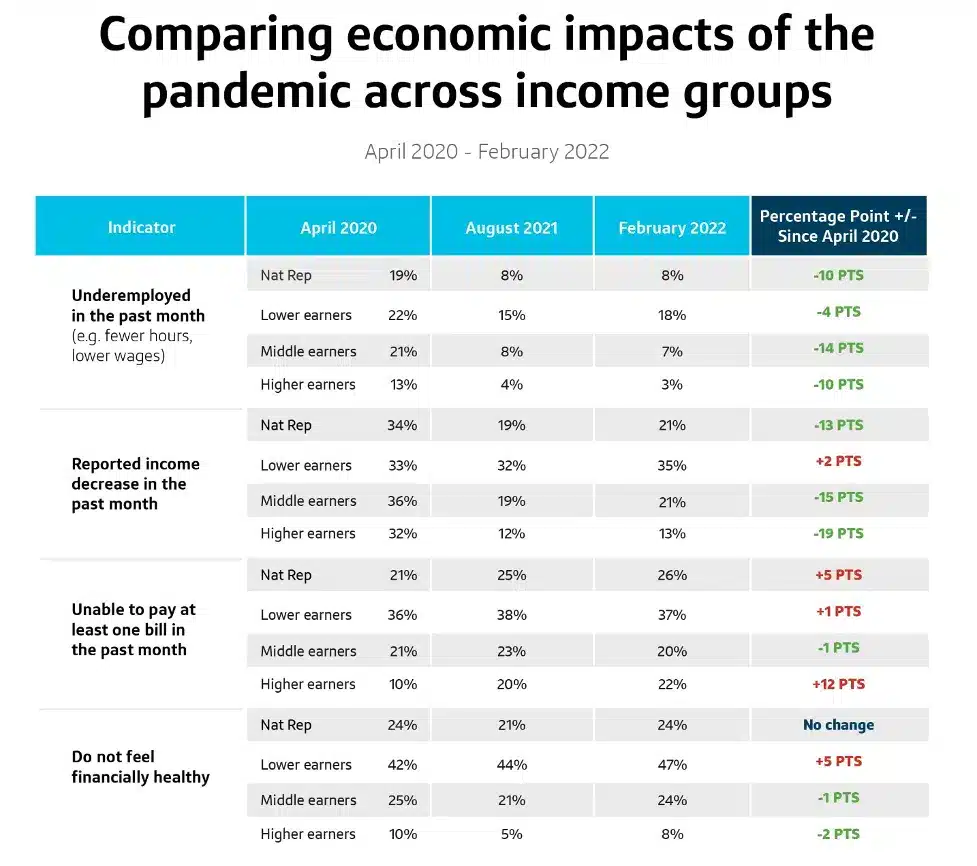

From the rise of the Omicron variant to the expiration of important government relief programs and stimulus, Americans have faced many new concerns, including soaring inflation. According to recent personal finance statistics, Millions of Americans' financial health has been strained, with lower-income workers bearing disproportionately dire consequences. When data from the early months of the pandemic is compared to February 2022, it demonstrates that:

- Underemployment: Compared to April 2020, underemployment (working less than preferred or for less money than before the pandemic) has improved significantly, although lower earners have not recovered at the same rate. Underemployment rates fell 14 percentage points for medium incomes (21 per cent in April 2020 vs. 7% in February 2022), 10 points for higher earners (13 per cent vs. 3%), and just four points for lower earners (Nat Rep: 22 per cent vs. 18 per cent) which resulted in consumer debt.

- Income: While fewer medium and higher incomes have reported income declines since April 2020, a somewhat higher proportion of poorer earners have reported further decreases (33 per cent in April 2020 vs. 35 per cent in February 2022).

- Bill payments: There has been a minor rise in Americans who were unable to pay part or all of their bills in the previous month across all income categories which include utilities, credit card debt, student loan debt, living expense and many more, since August 2021 (Nat Rep: 11 August 2021 vs. 13 per cent in February 2022), with lower incomes having the most difficulty (20 per cent vs. 22 per cent)

- Financial health attitude: Americans' perceptions of their present financial situation have deteriorated to early epidemic lows across income categories, mainly owing to the deteriorating sentiment among lower-income workers (42 per cent of lower earners reported that they do not feel financially healthy in April 2020 vs. 47 per cent in February 2022).

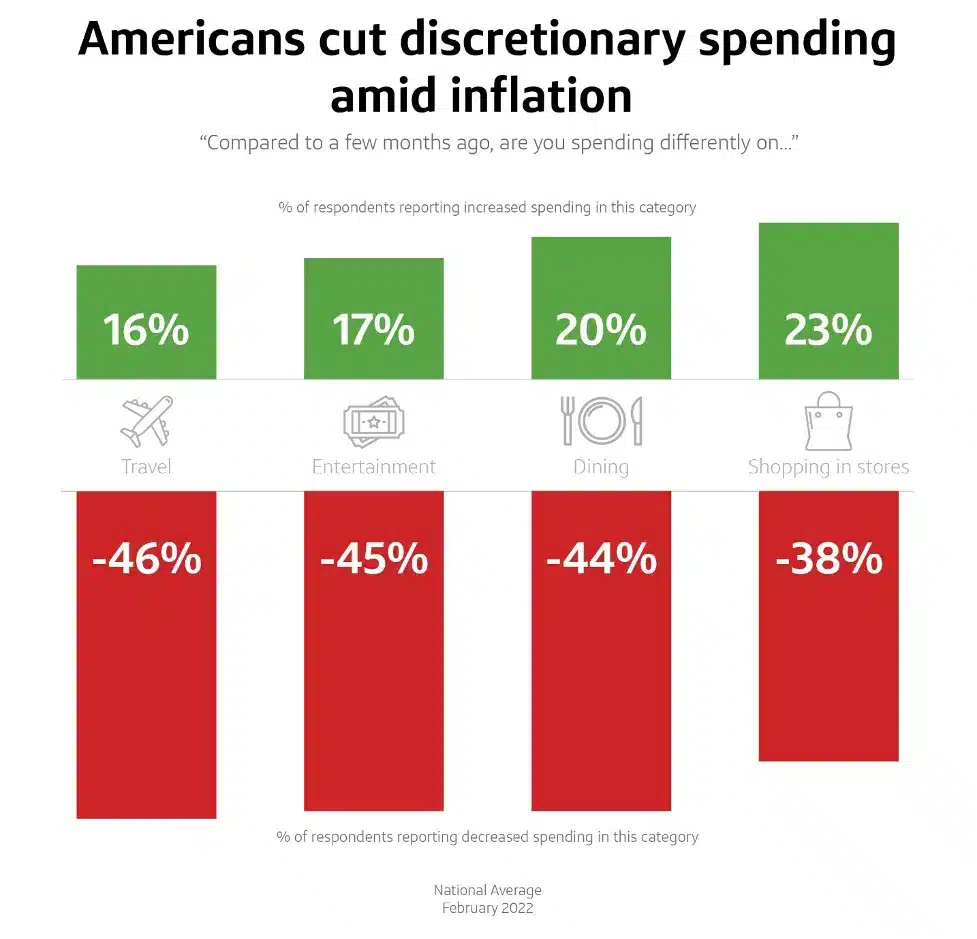

- As inflation fears grow, over six out of ten Americans say rising prices have impacted their spending, causing them to cut back on discretionary items. Most respondents (62%) said that inflation has lately affected living expenses, with lower and middle-income earners being the worst hit. As a result, compared to far lower rates among higher earnings, more than one-third of lower earners are making significant cuts to their travel, entertainment, and other living expenses (varying from 33-37 per cent across the categories above) (9-17 per cent).

- Some Americans turn to alternative financing sources, such as savings or borrowing, to offset growing prices. Nearly half of consumers (45%) took proactive steps to save money (e.g., cutting back on discretionary spending and cancelling/postponing trips). In comparison, more than half (58%) suffered a short-term financial setback (e.g., saving less, tapping into savings, borrowing money, taking out a loan).

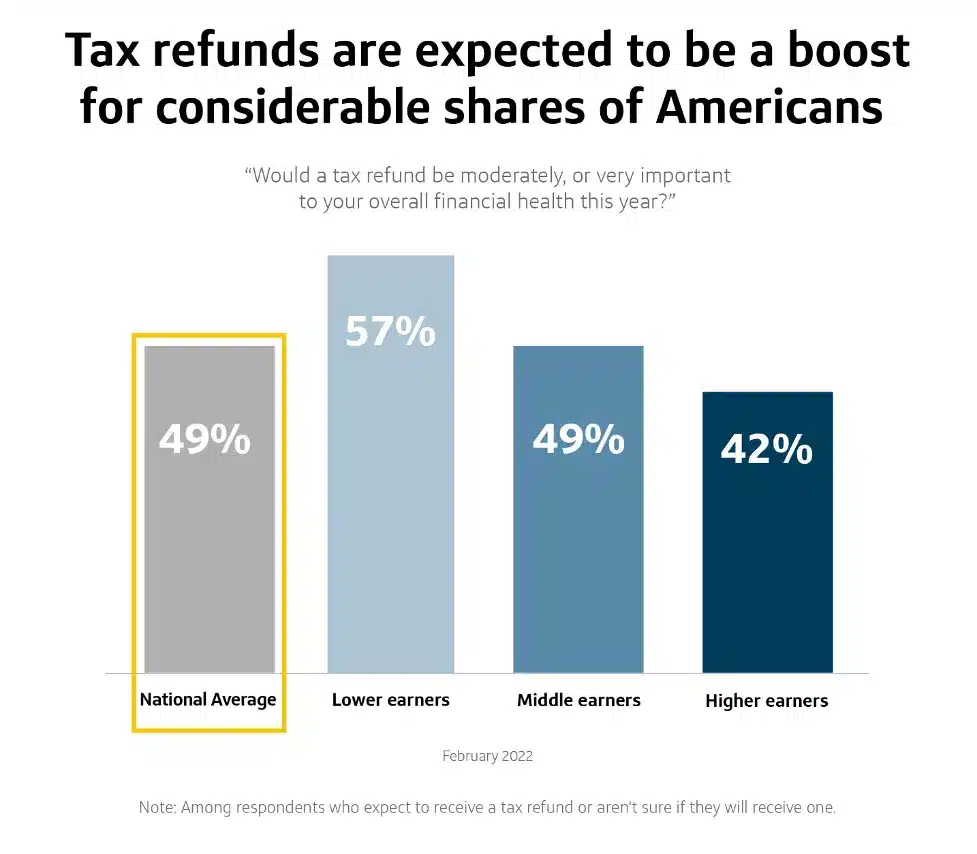

- Tax refunds are projected to provide a lift to many Americans. Nearly half of respondents (47%) expect a return after filing their 2021 taxes, with almost half of all lower-income respondents (43%) and three-in-ten middle-income respondents (30%) stating tax refunds are very or relatively significant to their overall financial health this year.

(Source: capital insight data centre till Feb 2022)

- Middle and higher incomes and a modest but considerable percentage of lower earners feel optimistic about their financial destiny. Eight out of ten higher payments anticipate being financially healthy in six months as of February 2022, compared to approximately six out of ten medium earners and around three out of ten lower earners.

What's the average debt of an American?

According to a new report by Nerdwallet, the typical American has roughly $155,000 in debt. This is an increase of more than 6% over the previous year. According to the same survey, most families' revolving credit card debt has decreased by about 14%. This implies you'll save around $100 in interest payments over the year.

While median wages have decreased by 3% in the last two years, living expense have increased by 7%. Many people are trying to make ends meet, especially with rising housing and medical costs. There are unavoidable costs that everyone must bear.

According to the Federal Reserve Bank of New York's quarterly report on household debt and credit, credit card balances climbed by $52 billion to $860 billion in the final three months of 2021, the highest quarterly gain in the data's 22-year history.

According to the New York Fed, total U.S. Average household debt climbed by $333 billion to $15.58 trillion in the fourth quarter. Debt balances, including mortgage, credit card, auto, and student loans, increased by $1 trillion in 2021, primarily due to mortgage liabilities.

Average Credit Card Debt in America 2022:

- National Statistics: The average credit card debt amount in the United States is $5,525 — down 6% year over year (Yoy). The average revolving utilization ratio in the United States is 25%, down 4% year over year. As of Q3 2021, the total outstanding credit card loans provided by FDIC-insured institutions was $806 billion, up 1% year over year.

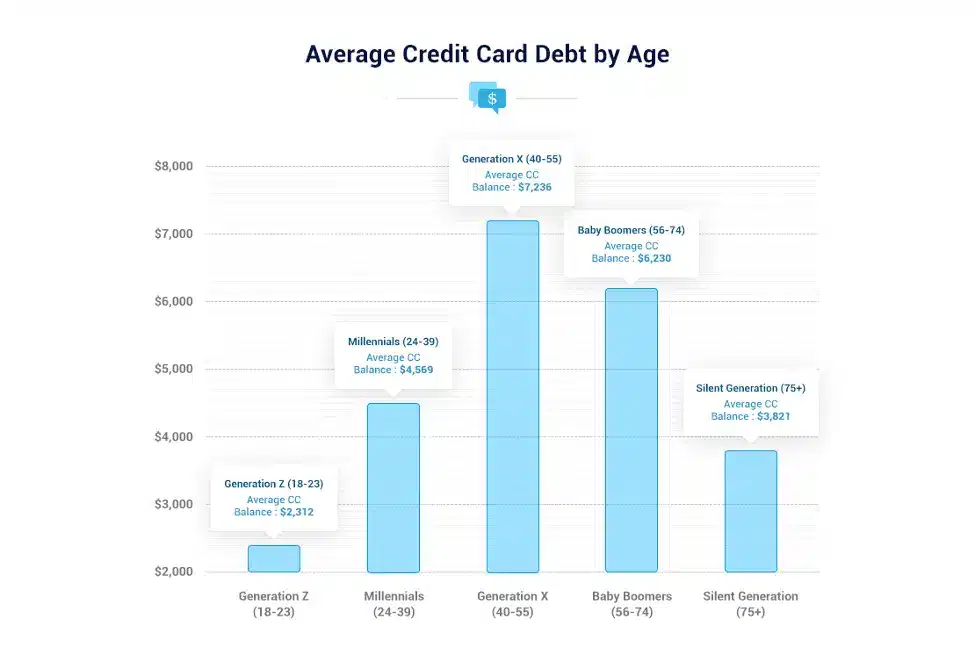

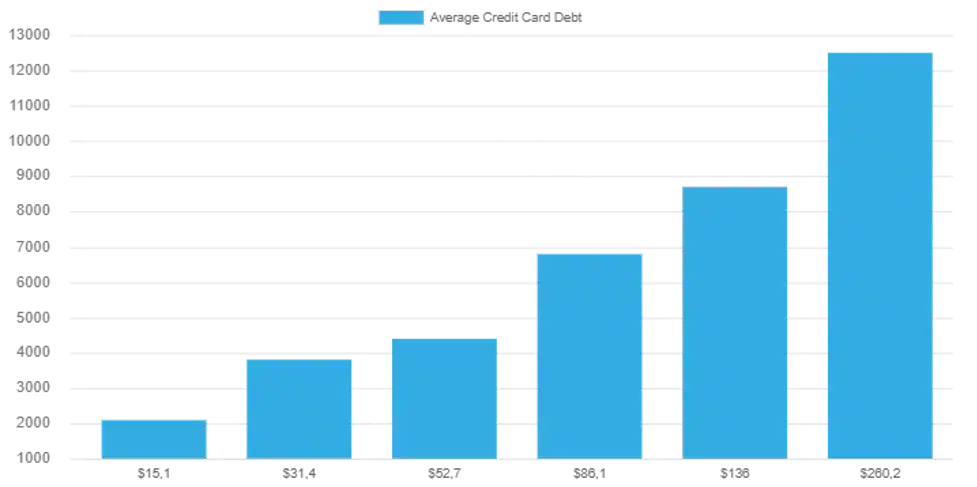

- Age: Generation X's average credit card debt amount ($7,236) is the highest, while the average credit card balance for Generation Z ($2,312) is the lowest.

The Silent Generation (12.6%) has the lowest revolving utilization ratio, while Generation Z (31.1%) has the most outstanding revolving utilization ratio.

Baby Boomers (3.4) have the most credit cards, while Generation Z (1.7) has the fewest. Credit card borrowers aged 18 to 39 (Gen Z and Millennial) have excellent delinquency rates among all age groups. According to figures issued Tuesday by the Federal Reserve's New York district, total U.S. consumer debt at the end of the year was $15.6 trillion, a year-over-year increase of $333 billion for the fourth quarter and just over $1 trillion for the whole year.

- Income: Americans' average credit card debt has a strong positive link with their median yearly salaries, as the living expenses increase, the average credit card debt for Americans with a median net worth income of $16,290 or less is $3,830. On the other hand, Americans with median net worth revenue of $290,160 or more have an average credit card debt of $12,600.

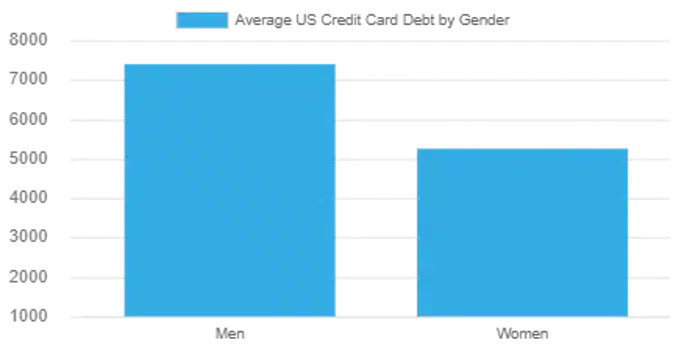

- Gender: American males' average credit card debt is $7,407, while American women's average credit card debt is $5,245.

- State: The most outstanding average credit card debt is found in Alaska ($5,388), Washington, D.C. ($5,118), and New Jersey ($5,034), while the lowest average credit card debt is found in Mississippi ($3,724), Kentucky ($3,826), and Vermont ($3,843).

The average credit card debt service coverage ratios (DSCRs) and Millennia’s average FICO Scores have an excellent association (0.74).

The greatest DSCRs are seen among millennials in Massachusetts (18.7), Washington, D.C. (17.6), and Connecticut (16.5). Unsurprisingly, the average FICO scores of Millennial in Washington, D.C. (715) and Massachusetts (710) are the second and third highest in the country.

The lowest DSCRs are seen among millennials in West Virginia (11), South Carolina (11.4), and Arizona (11.5). Furthermore, the average FICO scores of Millennial in South Carolina (656) and West Virginia (659) are the third and sixth lowest in the United States, respectively.

- Credit Card Interest Rates: In November 2021, national banks in the United States charged an average credit card interest rate of 14.51 per cent.

There are 497 million credit card accounts in the United States. In 2020, 12 million new credit card accounts will be established in the United States.

This figure was 21 million in 2019. The average number of credit cards per person in the United States is 3.0, which is the same as in 2020 and 2019.

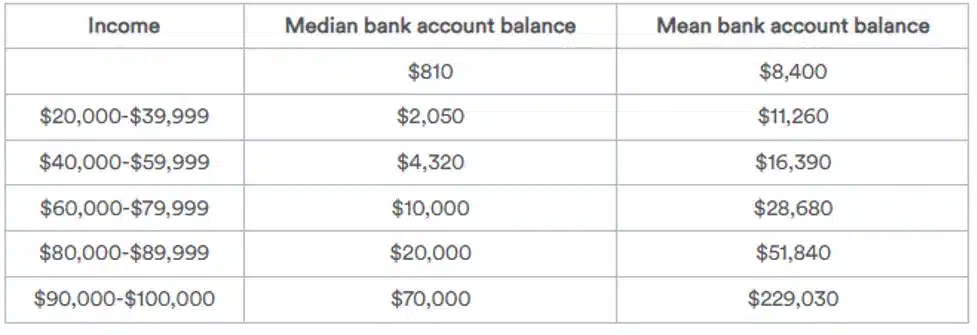

How much money does the average American have in the bank?

According to the most recent SCF money statistics, 98 per cent of American families have a transaction account, such as a savings account. Analysing the personal finance statistics if you have both savings and a checking account, you may move money automatically from one to the other to boost your savings.

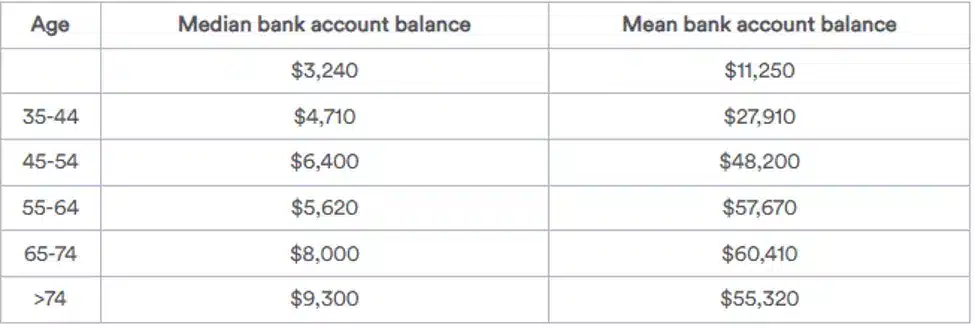

- Average Household Income and savings: According to the most recent SCF financial statistics, the median bank account balance is $5,300, while the average — or mean — value is $41,600. Because the average figure can be distorted greatly by a small number of outliers with large account balances, the median net worth balance may provide a clearer sense of how much most U.S. families have saved.

- Savings by age: Households income with senior members had bigger account balances — up to three times higher than those with younger members. On the other hand, households with members aged 45 to 54 had greater median net worth balances than those with members aged 55 to 63.

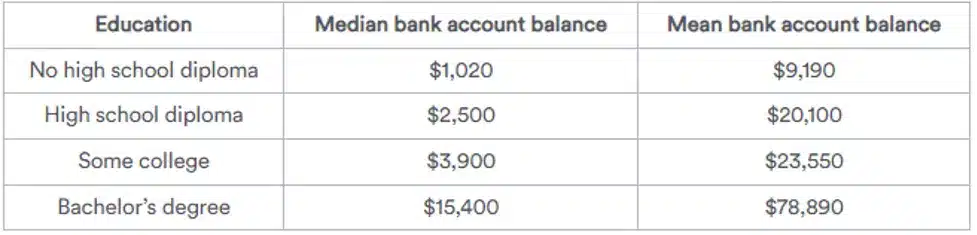

- Savings by education level: According to the SCF data, education levelis one of the criteria that connects with the bank account balance. The student loan debt balances change along with the amount of education that an individual has obtained. From those with some education ($3,900) to those with a bachelor's degree ($15,400), the median net worth balance jumps the most.

- Savings by income level: Income amount correlates with how much someone has in savings in the same way as age and education level do. Since the SCF research in 2013, the median net worth account balance for most income categories has steadily climbed. The research is carried out every three years.

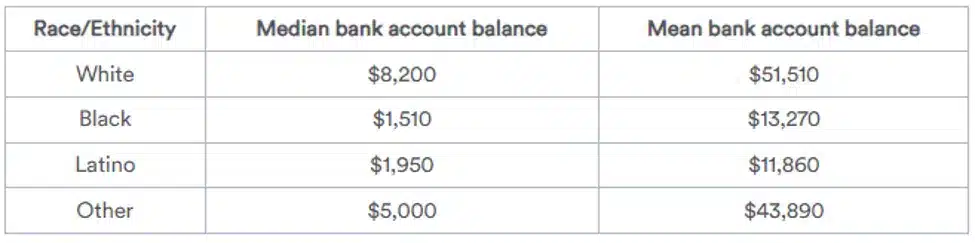

- Savings by race and ethnicity: In terms of race, non-Hispanic Whites and those classified as “other” had significantly higher median net worth and mean account balances than Hispanic and African American families, indicating a racial wealth gap, with White families owning eight times the wealth of the average Black family and five times the wealth of the average Hispanic family.

What are the five principles of personal finance?

According to money statistics 2022 data, people who do not save continue to spend. Unexpected life occurrences continue to occur. Without savings, a person is forced to borrow money for most unexpected emergencies, incurring interest and opportunity costs to financial institutions throughout his life. He will never be able to invest in the absolute greatest possibilities throughout his lifetime. He won't have any savings for the day he quits his work or becomes ill and loses his income. This is where the ancient proverb “he who fails to plan, plans to fail” comes into play.

The first saving question is, “How much should a person save?” We recommend that people save 15% or more of their income. This stage appears to be nearly hard for many individuals.

They have a bad tendency to spend whatever they earn, and often even more. If your client does not currently save at least 15% of their income, the Snapshot approach will assist in identifying chances to save more.

Encourage the notion of saving and increasing the percentage of money saved regularly. Clients should take advantage of every chance to save money. Like with any successful long-term program, effective tracking and measurement are critical. Personal Financial Snapshot provides the necessary monitoring.

1. Cut back on spending

This is by far the most crucial principle. You can only be successful if your monthly revenue exceeds your monthly costs. Spending less than you earn allows you to save money for the future rather than living pay check to pay check or falling further into debt because you can't pay your expenses. One legal piece of advice is to saving money at least 20% of your salary in a high-quality bank account. That's a reasonable aim for most individuals, but you should save even more. This will take rise your monthly money statistics.

2. Explore more sources of income

Although it is seldom discussed in personal finance, growing your income rather than cutting pennies is the easiest method to save more money.

You can save the amount of money by cutting back on your expenditures is limited. Sure, you can make a few cuts here and there, but that won't last. You'll eventually reach the point when no more cuts are to be made.

Instead of budgeting your way to wealth, you'd be far better off looking at financial statistics for and finding methods to create extra money and increase our median net worth. Negotiating a wage rise, finding a higher-paying job, freelancing, or beginning a side company is all methods to bring in extra money and have a better financial future

3. Putting money aside for a rainy day

Emergencies are unavoidable. They may be costly if you are not prepared for them. There are two approaches to preparing for unexpected expenses: Ascertaining if you have all of the appropriate insurance coverage, your emergency savings is the money you'll set aside to cover any unforeseen expenses. Your emergency savings should ideally include three to six months' worth of living costs. It takes time to save so much money, but it is better than none any money saved. Begin your emergency savings by creating a high-interest savings account and depositing as much as each month.

4. Improve your credit score

Whether you like it or not, your credit score dramatically influences your daily life. If you ever want to apply for one of the best credit cards or borrow money at a cheap interest rate, your credit score will be crucial. But that's not all it does: Your credit score can also influence your vehicle insurance rates, whether you have to pay a deposit when signing up for utilities or to hire for specific jobs. This is important for your financial future.

The good news is that it is not difficult to improve yours despite the uncertainty surrounding credit ratings. You'll need a credit card that you use and pay off each month to establish a track record of responsible borrowing.

5. Make retirement plans in advance

Retirement is also known as that thing that most people think about far later than they should. The sooner you begin contributing to a retirement plan, the better off you will be.

You must begin saving for retirement as soon as possible and take advantage of the tax advantages afforded by 401(k) s and individual retirement accounts (IRAs). You'll allow your money plenty of opportunities to grow through compound interest, which is the most effective approach to acquiring wealth.

What matters here is that you save money for retirement every month. Personal finance statistics showed whether its $50, $100, or more than $1,000, you'll be glad you started saving early. As long as you invest wisely in the financial future, your contributions will multiply several times over your career

Some quick stats to get you all motivated for a financial plan.

In 2020, Americans will have spent $415 billion due to a lack of financial literacy. The average credit card debt in the United States is $6,270.Approximately 40% of Americans have less than $300 in savings.

What percentage of people have a written financial plan?

What Exactly Is a Financial Plan?

A financial plan is a document that contains a person's present financial condition, long-term monetary goals, and tactics for achieving those goals. A financial plan is prepared individually or with the assistance of a professional financial planner and begins with a detailed review of the person's present financial situation and future aspirations. The recent personal finance statistics shows that:

- 58.1 per cent of millennials have savings totalling less than $10,000.

- Only 30 per cent of American households income have a long-term financial strategy.

- The average pre-tax family income in 2017 was $73,753.

- Americans spend 10.5 per cent of their income on food on average.

- Only 24% of millennials demonstrate basic financial knowledge.

- According to 2018 data, 39 per cent of Americans would struggle to handle an unexpected monetary bill of $400.

Most of us are aware that we should save money.

However, individuals are divided into two groups: non-planners and planners when it comes to implementing it. Non-planners often save when they can, maybe by contributing a tiny amount to a job retirement plan hoping that everything will work out in the long term. Planners often know what they're saving for, how much they need to keep, and how long it will take them to attain their objectives.

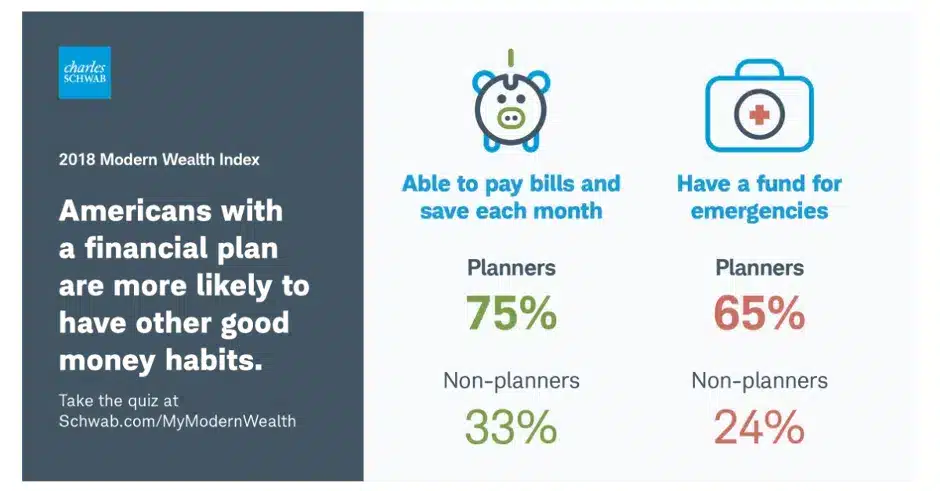

Is the first kind more similar to you? If so, you're not alone: according to Schwab's 2021 Modern Wealth Survey, just 33% of Americans had a documented financial plan.1 of the remainder, over half claimed they didn't have enough money to make a plan meaningful. Others claimed it was too difficult or that they didn't have time to devise a strategy.

Preparing for anything more than a few days ahead of time may be a hassle during daily life. It's reasonable to ask if financial planning is genuinely beneficial.

1. Having a documented financial strategy boosts confidence.

According to our poll of livin statistics, 65 per cent of those with a documented financial plan feel financially solid, whereas just 40 per cent of those without a plan feel the same way. Only 18% of non-planners were “extremely certain” they would meet their financial objectives, compared to 54% of planners.

A detailed financial plan provides you with a concrete target to aim toward. You can eliminate doubt or ambiguity about your decisions by measuring your progress.

Priorities must be established.

“People frequently believe there is too much knowledge available as a result of the Internet,” he remarked. “Many people are concerned that they may make a mistake due to an excess of information.”. This leads to lack of financial literacy.

According to Pearson, one method to overcome such apprehension is to first identify your financial priorities, such as creating targets for saving and debt repayment. Then, decide what measures you need to take to achieve those objectives. This is an effective way for better financial future plans

2. A financial plan may spark savings even with a tiny amount of money.

“I don't have enough money” is the most often mentioned excuse for not having a plan. This is a misunderstanding. Even in minor measures, planning does not require enormous quantities of money to begin.

Indeed, financial future planning may have a significant influence on low household income by assisting them in improving their saving and budgeting habits. A documented strategy assists savers in prioritizing their goals and, as previously said, gives a tool to measure performance.

3. A financial plan can assist you in developing an investment portfolio.

Your financial plan may provide you with the big picture: you'll know your goals, how much time you have to achieve them, you will have financial literacy and how risk-averse you are. You can figure out how to achieve each specific goal once you have a complete vision.

That will include saving—putting money away for the near term or emergencies—and investing, which is putting money aside for the long term and, hopefully, growing. And, with your financial plan as a guide, you'll be better equipped to make informed investment selections rather than winging it and hoping for the best.

4. A financial plan can help you develop healthier habits.

Financial planning is more than simply investing; it's about what money can do for your confidence, security, and quality of life, such as the protection provided by life insurance or the peace of mind offered by an emergency savings. According to research, planning also promotes good financial habits. There are healthy money habits and good investing habits. A documented financial plan can lead to both of these outcomes.

5. The habits of saving must be developed

While the median net worth savings rate is relatively high, many Americans struggle to save money. Recent economic issues have exacerbated the situation for some. According to The financial literacy statistics 2020 number represents a decline from the $400 in savings used by the Federal Reserve to gauge families' financial health the previous year.

When the poll results were broken down by gender, females outnumbered males in the $0-300 savings range. This might be an extension of the wage disparity between men and women.

References

- https://fortunly.com/statistics/personal-finance-statistics/#gref

- https://www.businesswire.com/news/home/20180515005598/en/Most-Americans-Don%E2%80%99t-Have-a-Financial-Plan-and-Many-Think-Their-Wealth-Doesn%E2%80%99t-Deserve-One

- https://www.schwab.com/resource-center/insights/content/does-financial-planning-help#:~:text=If%20so%2C%20you're%20not,Schwab's%202021%20Modern%20Wealth%20Survey.&text=Of%20the%20rest%2C%20almost%20half,time%20to%20develop%20a%20plan.

- https://youngandtheinvested.com/personal-finance-statistics/

- https://spendmenot.com/blog/personal-finance-statistics/

- https://www.goodfinancialcents.com/personal-finance-facts-and-statistics/

- https://mint.intuit.com/blog/financial-literacy/financial-statistics/

- https://savology.com/13-financial-statistics-you-need-to-know

- https://www.indiainfoline.com/article/news-top-story/10-basic-principles-of-personal-finance-114100400008_1.html

- 1. Cut back on spending

- 2. Explore more sources of income

- 3. Putting money aside for a rainy day

- 4. Improve your credit score

- 5. Make retirement plans in advance

- 1. Having a documented financial strategy boosts confidence.

- 2. A financial plan may spark savings even with a tiny amount of money.

- 3. A financial plan can assist you in developing an investment portfolio.

- 4. A financial plan can help you develop healthier habits.

- 5. The habits of saving must be developed